Note: The FxTR newsletter will take a break in the next two weeks. The weekly Fx analysis and the trade ideas will return from the week starting on August 29.

It’s mid-year 2022, and it’s time for an update on the US dollar and what lies ahead for the coming months. In this special edition of the FxTR newsletter, we will look at the long-term prospects for the USD trend and, in particular, how high it can go before it eventually peaks.

The USD strengthened markedly this year, particularly following the outbreak of the Russia-Ukraine war and the imposing of sanctions by the West on Russia (triggering the energy crisis). The USD bull trend is powerful, and currently, no one is willing to stand in the way and take a bet against the mighty dollar. Indeed, the most likely scenario for the coming months is further USD strength as the Fed stays resolutely hawkish to fight the biggest inflation threat the world has seen in 40 years.

However, the outlook for the Forex market is less clear beyond a few months forward (year-end). That is mainly because of the global and geopolitical factors that are now mainly in the driving seat of financial markets, which are very hard to predict or forecast. Thus, developments related to the war in Ukraine and relations with Russia will continue to be a big factor in the Fx market. There is now a focus also on China and Taiwan, and escalation there could quickly rattle markets like the Russian actions in Ukraine did in February.

With that being said, the Fx market always resorts to trading on what matters to it most. It is a relative game, and the currencies of countries with better relative economic prospects tend to strengthen against currencies with worse relative economic prospects. It is as simple as that on the long-term horizon. This is playing throughout this year as the financial markets are perceiving the United States and the dollar as the safest place to be in the face of the European energy crisis, high oil prices, the war in Ukraine and incoming recession risks. These are global factors of longer-term nature, and unfortunately, the war in Ukraine or the energy crisis are unlikely to get a clear and quick resolution - This is why the USD uptrend since February has been so stable and why most Fx market participants expect further USD strength this year.

Europe with and without the cheap Russian gas is not the same. It used Russian gas to pretty much run the engines of its economy. That is no longer the case, and Europe’s economic prospects became much worse overnight. Thus, financial markets adjusted significantly, with EURUSD hitting the parity level (1.00). The fall in EURUSD is not temporary, but more likely a long-term adjustment lower that will linger for longer.

When will the Dollar Peak? – Look at Inflation

Of course, inflation is the other big theme that is gaining the most attention. It has caused central banks to pivot policy abruptly and embark on the swiftest tightening cycle in decades. The Fed tightening is already very aggressive, having raised rates to 2.5% last month. More is in the pipeline as QT will accelerate, and more rate hikes will be delivered.

Inflation is high now, but is it going to last? – The answer is most likely not. The bond market, which is historically the best predictor of future inflation, thinks it will not last. For instance, long-term bond yields like the 10-year and 30-year Treasuries trade around 3%, where they have been for most of the time in recent years. If inflation would stay persistently high (say at 8%), those bond yields would be trading near to and above that 8% level. But they aren’t. Hence, the bond market has a conviction that inflation will go back toward the 2% Fed target, and it is likely to be proven correct (as it has been in most cases in the past).

The only problem is that central banks will bring down inflation by bringing down the economy too. A global recession in a few months from now is a real possibility, while in European countries, it is a certainty (as the Bank of England already admitted and the ECB will soon have to as well). Based on this, we can say that the US dollar could peak when inflation starts to fall notably and the Fed changes to a less hawkish or outright dovish stance. It may seem like a distant scenario, but it doesn’t have to be, as economic factors can change quickly.

Considering the projected path of Fed rate hikes and the forecasts for the economy, inflation has likely already peaked while recession could hit hard in a few months from now. This means that somewhere between 3-9 months from now, we could see the end of the Fed hawkishness and a big shift to a dovish stance due to inflation falling and economic growth slowing sharply.

Thus, some further straightening of the dollar could take the DXY index another bullish leg higher where it could peak for this cycle. Based on the technicals (see above), this could happen some time during the autumn months in the 112.00 - 114.00 area on the DXY chart.

Russia and the war in Ukraine as the main drivers of both EUR weakness and USD strength

A stronger dollar means a lower EURUSD, as the euro has a 57.6% weight in the DXY index. So, further USD strength means that EURUSD will break below parity (1.00) and likely stay there for some time. The exact path for EURUSD will depend a lot on how things go with Russia, and specifically the gas and electricity energy crisis. The worse the energy crisis in Europe gets, the lower EURUSD will trade.

From the current perspective, the current global geopolitical landscape could develop in three directions.

Consequently, there would be three scenarios for the Fx market:

1) The USD stays strong - Essentially, as long as things stay as they are (or worsen), the USD will stay firm. That is, the Ukraine war continues, sanctions on Russia remain, and the Fed stays more hawkish than other central banks.

2) The USD weakens sharply - For a reversal scenario, we need a reversal of some of these factors. That would mean a significant softening or an outright end to the war and sanctions on Russia, which would also put an end to the energy crisis. Under such a scenario, the US dollar will likely see a big correction down as the euro and other beaten-down currencies rally in relief. Nonetheless, this still looks like a highly improbable scenario for the time being, but one that has to be kept at the back of our minds simply because it can unleash huge moves in the markets.

3) The dollar trend slowly turns around - Another scenario that must be considered is the “grey” one – in the middle between the previous two more extreme scenarios. If the worse of the Ukraine war is already behind, even if things don’t improve materially and simply stay in a status-quo state (e.g., irregular and moderate skirmishes in Ukraine), the markets may start to care less about those events. This could see a gradual reversal of the Fx trends from this year, resulting in a moderately weaker USD. But such a scenario would unfold very gradually, and currently it is still too early to suggest that

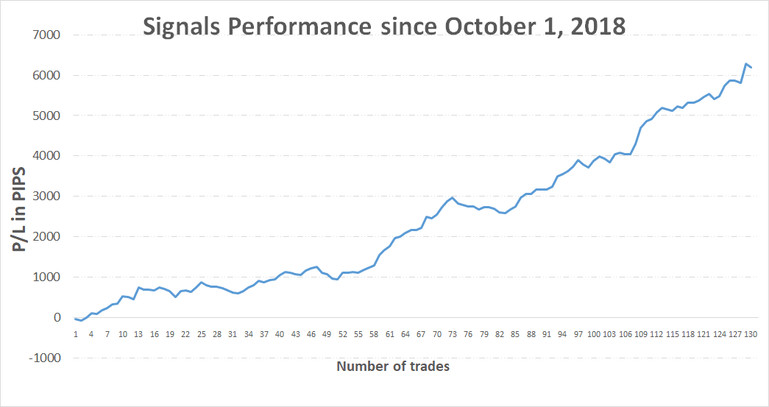

Trade signals from the past weeks

- August 4, 2022 - Short AUDUSD from 0.6970, stopped out today (Aug 10) at 0.7050 = -80 pips

TOTAL P/L in the past week: -80 pips

TOTAL: +6195 pips profit since October 1, 2018