As we suggested in yesterday's article, Fed Chairman Jerome Powell again attempted to calm the markets, reiterating that, despite the sharp rise in inflation, it is too early to consider tightening financing conditions, and there is still a long way to reduce asset purchases.

Speaking on Wednesday before the House of Representatives Finance Committee with a semi-annual report on monetary policy, Jerome Powell said that the state of the American economy has improved, but significant additional progress has not yet been made in this direction.

Despite the fact that the US inflation data released on the eve of Powell's speech turned out to be higher than expected (the consumer price index CPI rose in June by +0.9% (+5.4% on an annualized basis), and inflation expectations jumped to 4.8 % (from 4% in May), which is a record high), he continues to insist that inflationary pressures will ease later this year.

The dollar fell immediately after Powell's speech, however, this decline cannot be called strong. The DXY dollar index is still holding above 92.00, maintaining positive dynamics and readiness for further growth.

The Fed is closer to normalizing policy than other major world central banks, in particular the ECB and the Bank of Japan (the share of the euro and the yen in the DXY dollar index is more than 70%). Given the growing inflationary pressure in the United States, the Fed will sooner or later begin to wind down its stimulating policy.

Against the general background, the British pound also looks relatively attractive. It rose on Wednesday after the release of data released by the National Bureau of Statistics showing that annual consumer price inflation in the UK climbed to 2.5% in June, while economists had forecast a rise of 2.2%, the highest annual growth since the summer 2018. Thus, for the second month in a row, inflation has been above the Bank of England's target of 2.0%.

Some economists predict that inflation will peak at slightly above 3% at the end of the year, with food and energy prices rising the most.

At the same time, according to economists, the Bank of England is still inclined to ignore the acceleration of inflation and wait for the completion of employment support programs in order to assess the consequences of the pandemic on the labor market. The Bank of England has already announced that inflation exceeding 2% will be temporary.

However, given the relative stability in the labor market, it can be assumed that in the near future the leaders of the Bank of England may start discussing the curtailment of quantitative easing measures.

Today, the UK National Statistics Office released data showing that the unemployment rate for the three months ended in May was 4.8%, higher than the similar figure of 4.7% in April, but below the 5% in February. At the same time, earnings growth in the UK accelerated in May to 6.6% from 5.7% in April. Thus, while the labor market has not yet fully recovered from the impact of the Covid-19 pandemic, earnings have already risen above the pre-crisis trend, exacerbating inflationary pressures.

At the same time, the number of staffed jobs in British companies in June increased for the seventh month in a row, and the number of vacancies again exceeds pre-crisis levels. This means that unemployment will continue to fall, economists say.

Thus, the Bank of England is also rapidly approaching the moment when, given the improvement of the labor market and its reaching pre-crisis levels, as well as the growing inflationary pressure, it will be forced to start phasing out its stimulus policy, and this is a strong factor already being pledged by many investors into prices pushing the pound up.

The pound is currently also supported by the readiness of the British authorities to lift quarantine restrictions on July 19, despite the active increase in the incidence of a new strain of coronavirus (the government believes that the vaccination campaign of the population continues at an active pace, and the number of hospitalizations and overall mortality are at controlled levels).

Michael Saunders, a member of the Bank of England's Monetary Policy Committee, said today (at 10:00 GMT) that "the question of whether the current program of asset purchases should be canceled ahead of schedule will be considered at upcoming meetings". "Activity appears to have rebounded slightly faster than forecast in May", Sanders added, and "options for removing stimulus include reducing quantitative easing (ending in the next month or two) and / or further policy action next year".

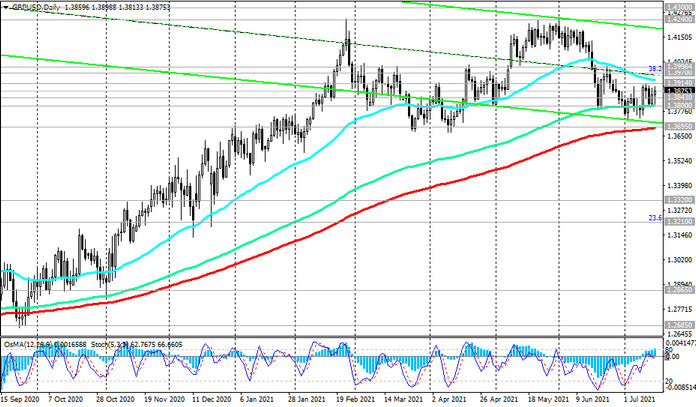

The pound strengthened sharply after these words of Sanders, and the GBP / USD pair jumped 60 pips in the moment, to an intraday high of 1.3898, also generally maintaining positive dynamics.

As for the dollar and the GBP / USD pair, respectively, market participants will pay attention to the publication at 12:30 (GMT) of weekly data from the US labor market (another decrease in the number of initial jobless claims is expected) and to the second speech by Jerome Powell in Congress (at 13:30 GMT). However, it is unlikely that he will surprise the markets with anything today after his speech yesterday.