Despite a rather sharp strengthening of the pound at the beginning of today's European session, the DXY dollar index is still growing since the beginning of today (as you know, the pound's share in the DXY dollar index is about 12%). DXY futures are traded near 95.52 as of this writing, in close proximity to the local 16-month high of 95.59 hit on Monday. Market participants are betting on further strengthening of the dollar, expecting a more rapid tightening of the Fed's monetary policy after the release of strong inflation data.

The dollar is actively strengthening against its main competitors in the foreign exchange market, primarily against the euro (its share in the DXY dollar index is about 58%).

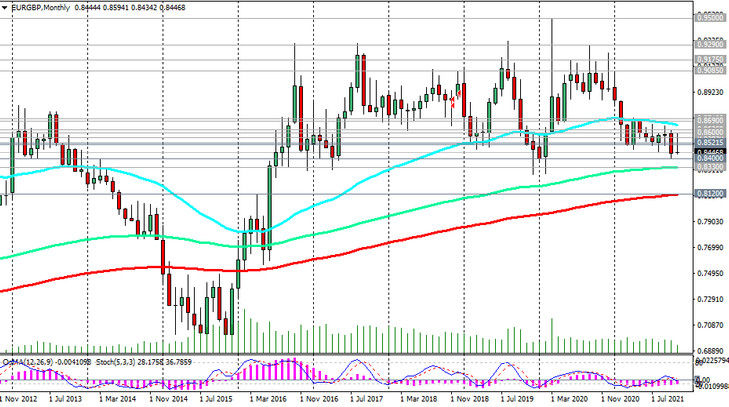

Accordingly, the pair EUR / GBP has dropped sharply today, amid the strengthening of the pound and the continuing weakening of the euro.

The strengthening of the pound today was facilitated by the data from the British labor market, published in the morning by the National Statistics Office of Great Britain. According to the report, the number of employed Britons increased in October (the number of jobs in the country amounted to 29.3 million, 160,000 more than in September), and their salaries increased.

Thus, average earnings (excluding premiums) in July-September increased by 4.9%, with premiums - by 5.8%, and unemployment over the same period decreased to 4.3% (against the forecast of 4.4% and 4.5% in the previous period).

Thus, the presented data speaks in favor of an imminent increase in the key interest rate by the Bank of England, possibly already in December. In addition, Bank of England Governor Andrew Bailey told British lawmakers on Monday that he was “very worried” about rising inflation and that the central bank’s decision to keep rates unchanged earlier in November was not unanimous.

Meanwhile, economists and market participants do not expect similar actions from the ECB. Most of them believe that the ECB will maintain a soft policy longer than other major world central banks. The ECB will likely even increase the volume of the Asset Purchase Program (APP) from 20 billion to 40 billion euros per month when the Emergency Asset Purchase Program (PEPP) ends in March. The main interest rates of the ECB, at the same time, will remain at the same level until 2025, some economists say.

Concerns about the outlook for the Eurozone economy, triggered by rising energy prices, rising coronavirus cases and slowing activity in China, are prompting a buildup of short positions in the euro. European Central Bank Governor Christine Lagarde said Monday that tightening monetary policy to curb inflation could seriously slow the eurozone's economic recovery. Although inflation in the Eurozone has already doubled the target levels, according to Lagarde, conditions for a rate hike are unlikely to emerge before 2023.

Economists anticipate a slowdown in Eurozone economic growth in the 4th quarter of 2021 as the momentum from company resumptions fades, the number of new coronavirus infections in some Eurozone countries rises, and widespread supply problems negatively affect the region's manufacturing sector.

Market participants are also monitoring the progress of trade negotiations between the UK and the EU. UK government officials said yesterday that they remain hoping for a consensus on commodity checks at Northern Ireland's borders. Most likely, the UK will not agree to a unilateral withdrawal from trade agreements.

Thus, we should expect further weakening of the euro and the fall of the EUR / GBP pair.

The closest support level and the closest target of the EUR / GBP decline are near 0.8400 (last month's lows), while more distant ones are near 0.8330 and 0.8120 (see Technical Analysis and Trading Recommendations).