The ADP report on employment in the private sector of the American economy, published on Wednesday, somewhat puzzled market participants. The DXY dollar index fell yesterday to a new intra-week low of 95.80, while the 10-year US Treasury yield fell about 3 basis points to 1.77%.

According to this report, the number of jobs in the US private sector decreased by 301,000 in January, the sharpest drop since April 2020. Economists predicted an increase in their number by 207,000. In the service sector, the number of jobs decreased by 274,000, in the manufacturing sector, the number of jobs decreased by 27,000.

This is certainly disappointing data, which reflects, in particular, the negative impact of the omicron strain of coronavirus, as many workers are forced to go on sick leave and self-isolate.

The ADP data may differ significantly from the Department of Labor data, however, it is often seen as a precursor to official data. They will be published tomorrow at 13:30 (GMT). Economists expect the data to show 150,000 new US non-farm payrolls in January, up from 199,000 in December. At the same time, forecasts differ significantly, and many economists believe that employment during the reporting period could have declined.

Nevertheless, economists believe that the deterioration of the labor market is unlikely to affect the Fed's determination to raise interest rates: the effect of a new wave of the disease is likely to be temporary, but accelerating inflation in the United States is really alarming.

In connection with the forthcoming publication of the US Department of Labor report on Friday, today market participants and economists will pay attention to the publication (at 13:30 GMT) of weekly statistics on the dynamics of initial and repeated claims for unemployment benefits. Initial jobless claims are expected to fall to 245,000 after their unexpected rise to 260,000 the week before last and to 290,000 three weeks earlier. Despite the growth, this is still a low number of applications for unemployment. It remains at the lowest level for several decades - about 200 thousand. At the same time, unemployment in the country is at the minimum pandemic and long-term level of 3.9%.

Among other important macro data for the dollar, the publication at 15:00 (GMT) of data on manufacturing orders in December and business activity in the US services sector in January should be noted. The PMI index of business activity (from ISM) in the services sector assesses the state of this sector in the US economy. They, unlike the manufacturing sector, have virtually no impact on the country's GDP. Forecast for January: 59.5 (after rising to 62.0 in December), which is likely to have a generally positive impact on the USD, despite the relative decline in the indicator.

A result above 50 is seen as positive for the USD. However, a deeper relative decline in the index, and especially below the value of 50, may negatively affect the dollar in the short term.

Meanwhile, at the same time tomorrow (13:30 GMT), Statistics Canada will release its monthly employment report. Unemployment has risen in Canada in recent months, partly amid massive coronavirus-related business closures and layoffs. Unemployment rose from the usual 5.6% - 5.7% to 7.8% in March and already to 13.7% in May 2020. If unemployment continues to rise, the Canadian dollar will decline. If the data turns out to be better than the previous value, then the Canadian dollar will strengthen. Decreasing unemployment rate is a positive factor for CAD, rising unemployment is a negative factor. In August, unemployment was at 7.1%, and in December 2021 it was 5.9% (against 7.5% in July, 7.8% in June, 8.2% in May, 8.1% in April) . According to the forecast, unemployment in Canada is expected to rise to 6.2% in January, while the number of employees decreased by -117.5 thousand. This is negative data for the CAD, whose quotes may decline, especially against the backdrop of moderately declining oil prices.

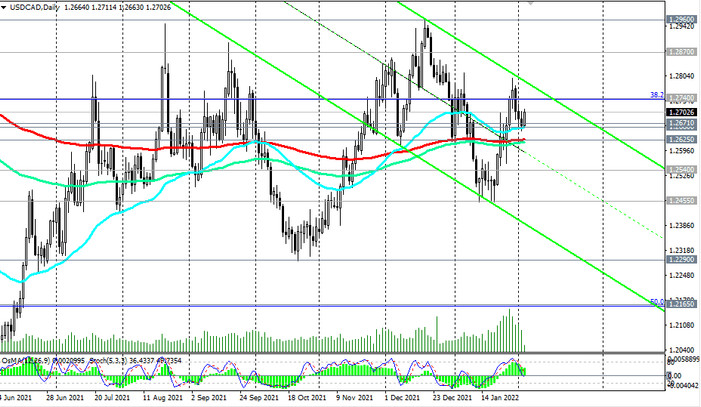

Thus, on Friday at 13:30 (GMT) a sharp increase in volatility is expected in the financial markets and, first of all, in the USD quotes and in the USD/CAD pair. If the official data of the US Department of Labor are disappointing, then this is likely to be followed by a weakening of the US dollar and a decrease in USD/CAD. However, the weakening of the US dollar is likely to be short-lived.

While investors are now expecting a less aggressive Fed tightening after yesterday's ADP report (some of them quoted 5 or more rate hikes this year and a 0.50% rate hike in March), this ADP report and tomorrow's Department of Labor report will most likely be ignored by Fed leaders.

As early as last week, when the Fed's January meeting ended, its head Powell said that "the economy is in very good shape, inflationary pressure is high, so it is advisable to consider postponing (plans) to curtail asset purchases a few months earlier".

From the results of the January meeting of the Fed, it follows that the US central bank will overtake other major world central banks in the process of tightening monetary policy, and the divergence of the curves reflecting the dynamics of monetary policies will increase over time. And this is one of the most important factors in favor of further strengthening of the USD, if, of course, the Fed manages to quickly cope with rising inflation as a result of these actions.